How Filings-Based Pricing Engines Are Transforming Insurance Product Delivery

A deep dive into how insurers are accelerating product launches, improving governance, and owning their pricing logic with modern enterprise rating technology.

The way insurers build, launch, and manage pricing is undergoing its fastest evolution in decades. With regulatory filings growing ever more detailed, digital distribution scaling faster than internal systems, and competitive pressure increasing every quarter, insurers are being pushed to operate with a level of agility that legacy rating engines simply cannot support.

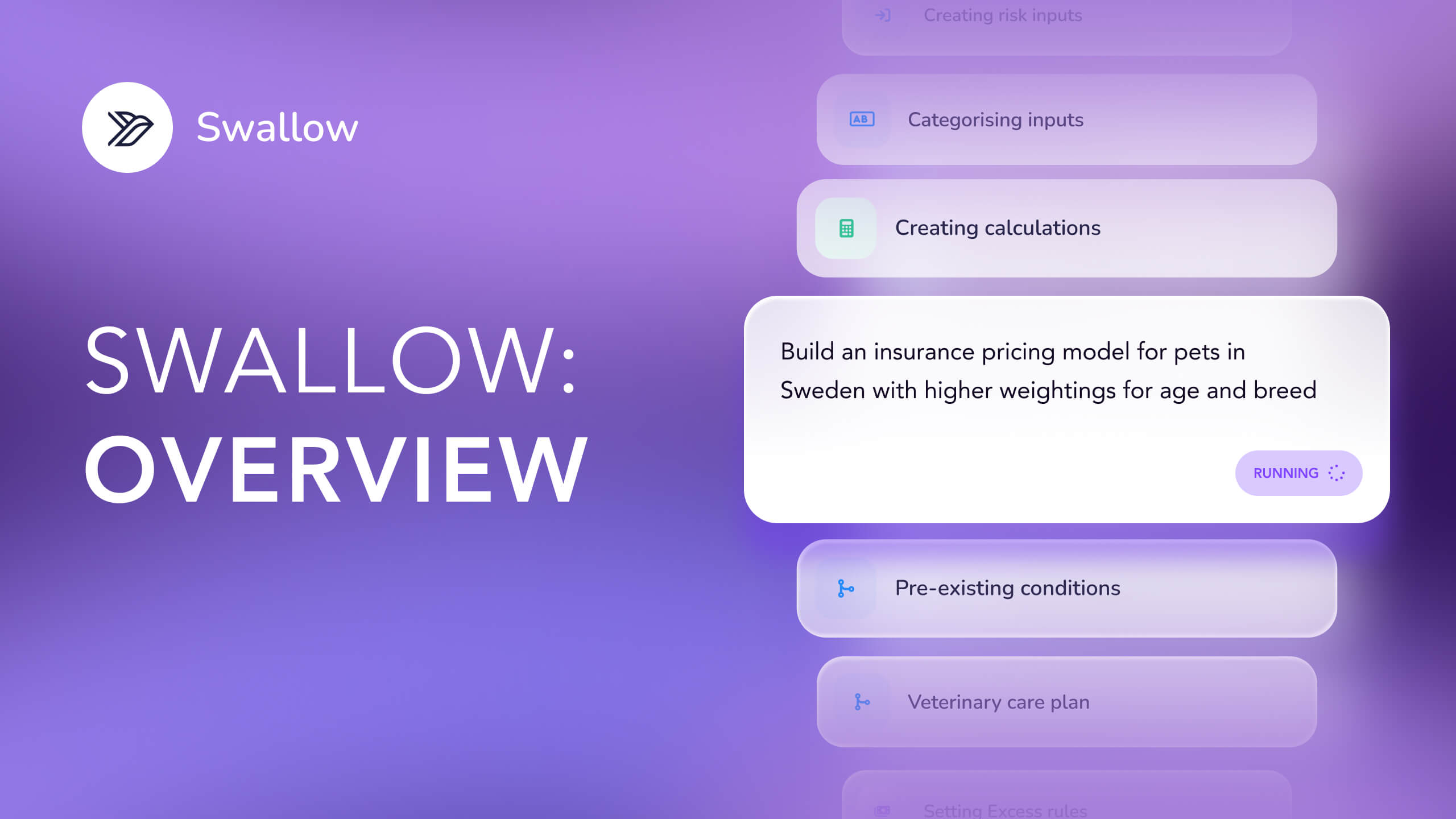

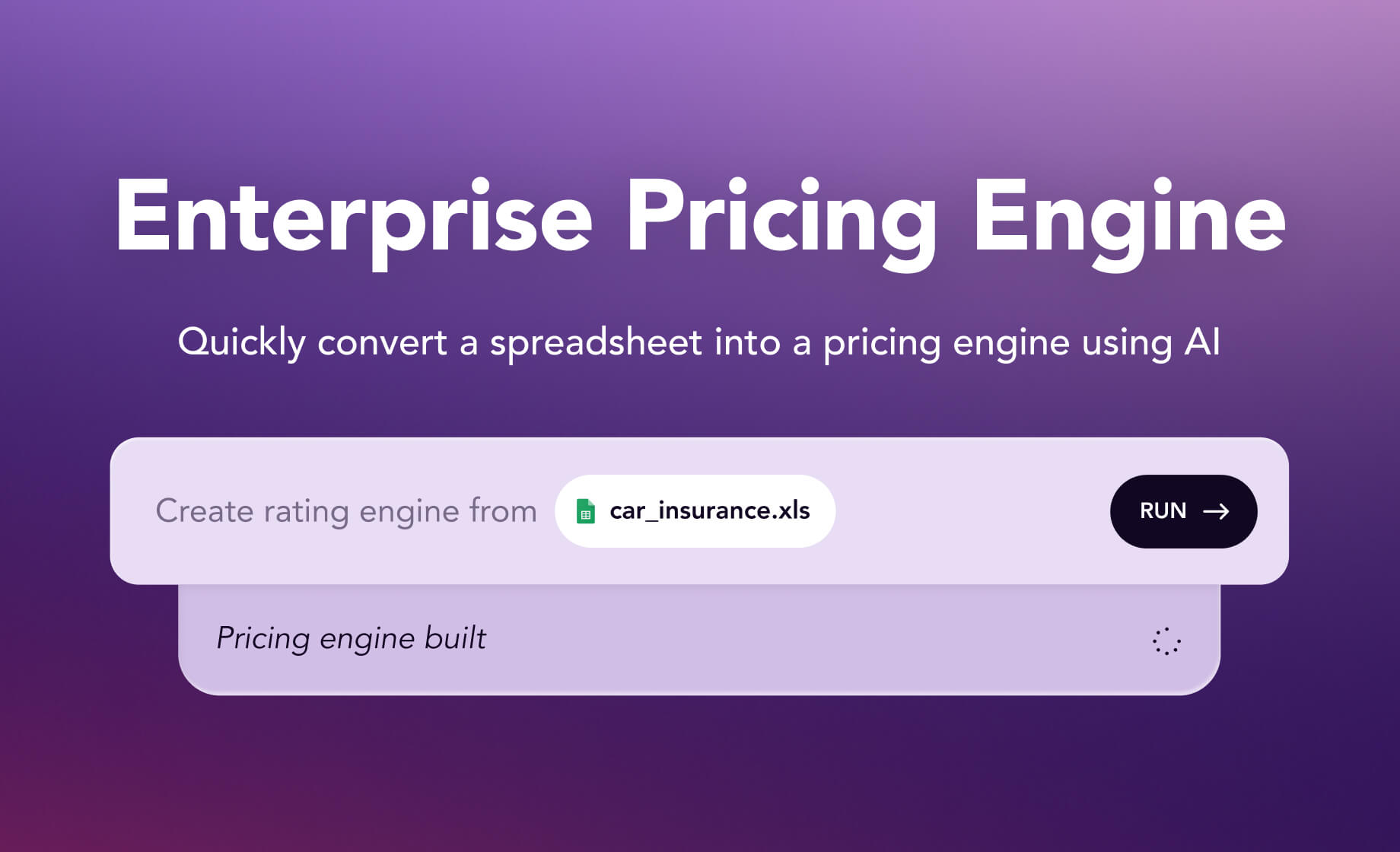

A new generation of pricing engines is emerging to solve exactly that problem. One of the most powerful examples is Swallow’s filings-based “me-too” pricing engine — a system that converts public filings into live, production-ready rating APIs while sitting inside a fully modern enterprise rating stack.

This article explores how this model works, why insurers are adopting it at speed, and what it means for the future of enterprise pricing.

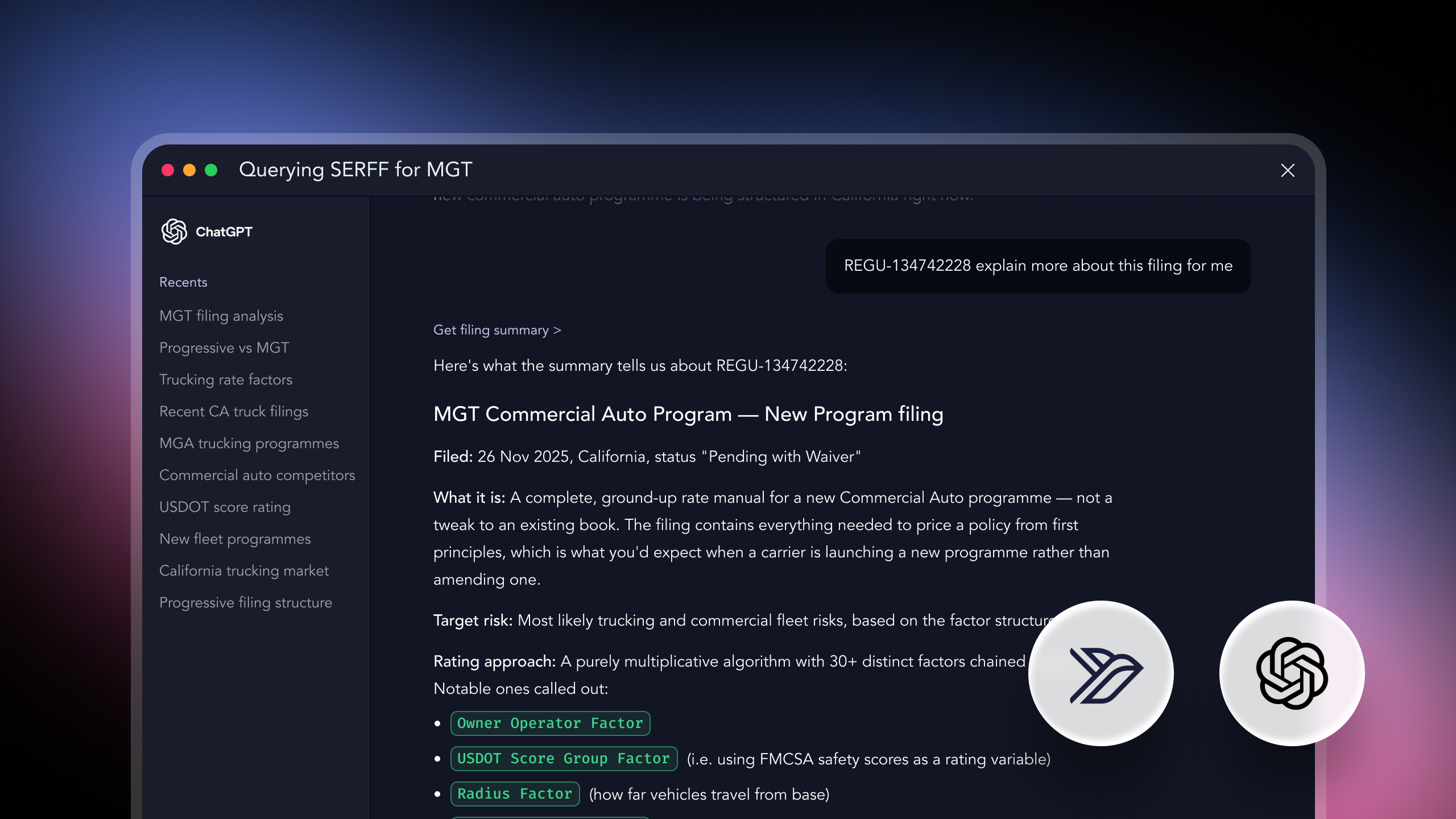

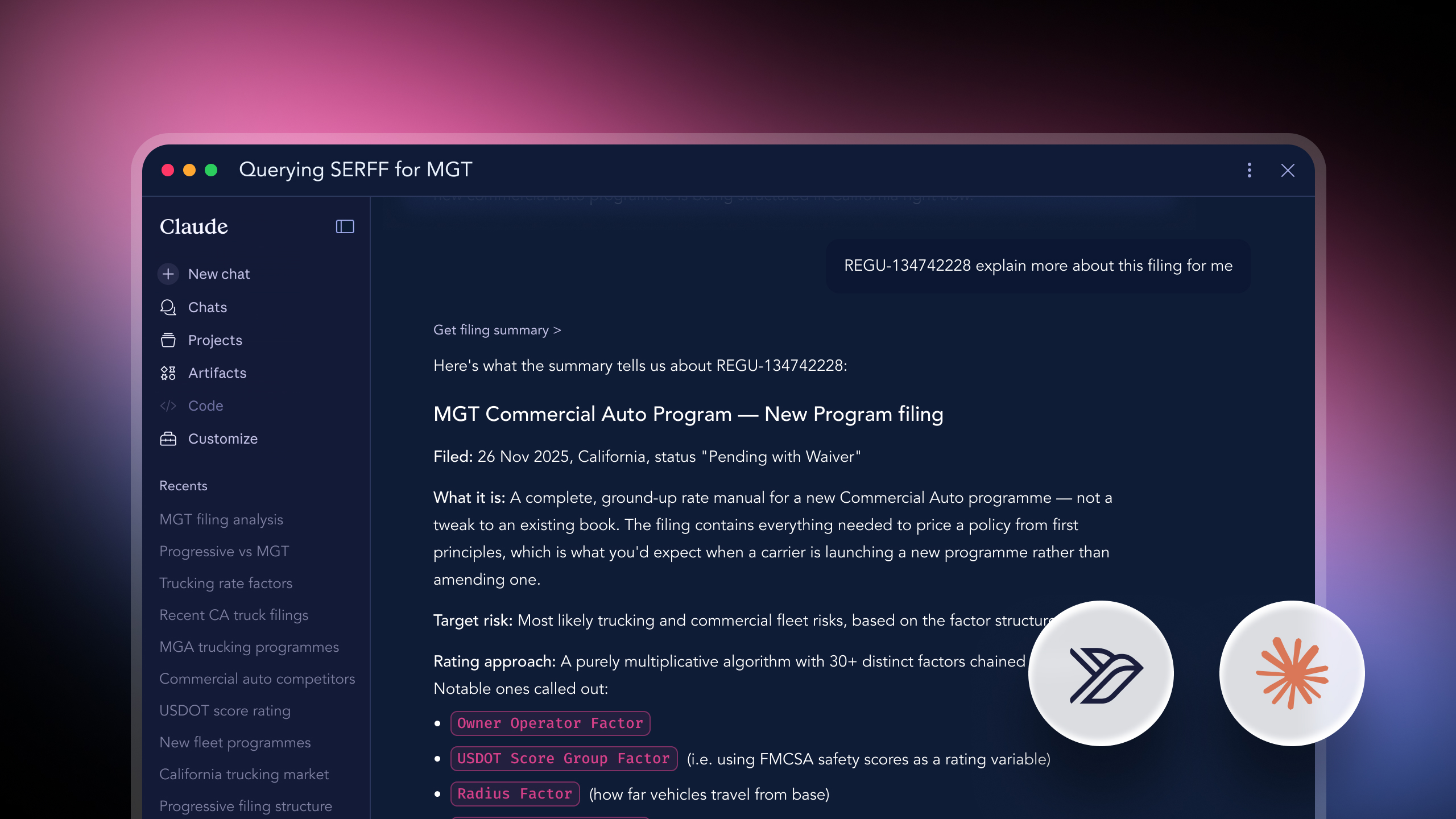

Public regulatory filings — such as SERFF, ISO, AAIS, and bureau updates — already contain an enormous amount of actuarial intelligence. But historically, extracting that information has been a slow, manual process involving re-keying, cross-checking, and rebuilding models from scratch.

A filings-powered engine removes this burden. Instead of spending weeks deciphering documents and assembling rating tables, teams can generate a complete, editable pricing model directly from the filings themselves.

That means:

For many insurers, this single capability cuts months off product lifecycle timelines.

The filings workflow is only one part of the system. What really unlocks value is that it sits inside a full enterprise-grade pricing engine designed for speed, governance, and scale.

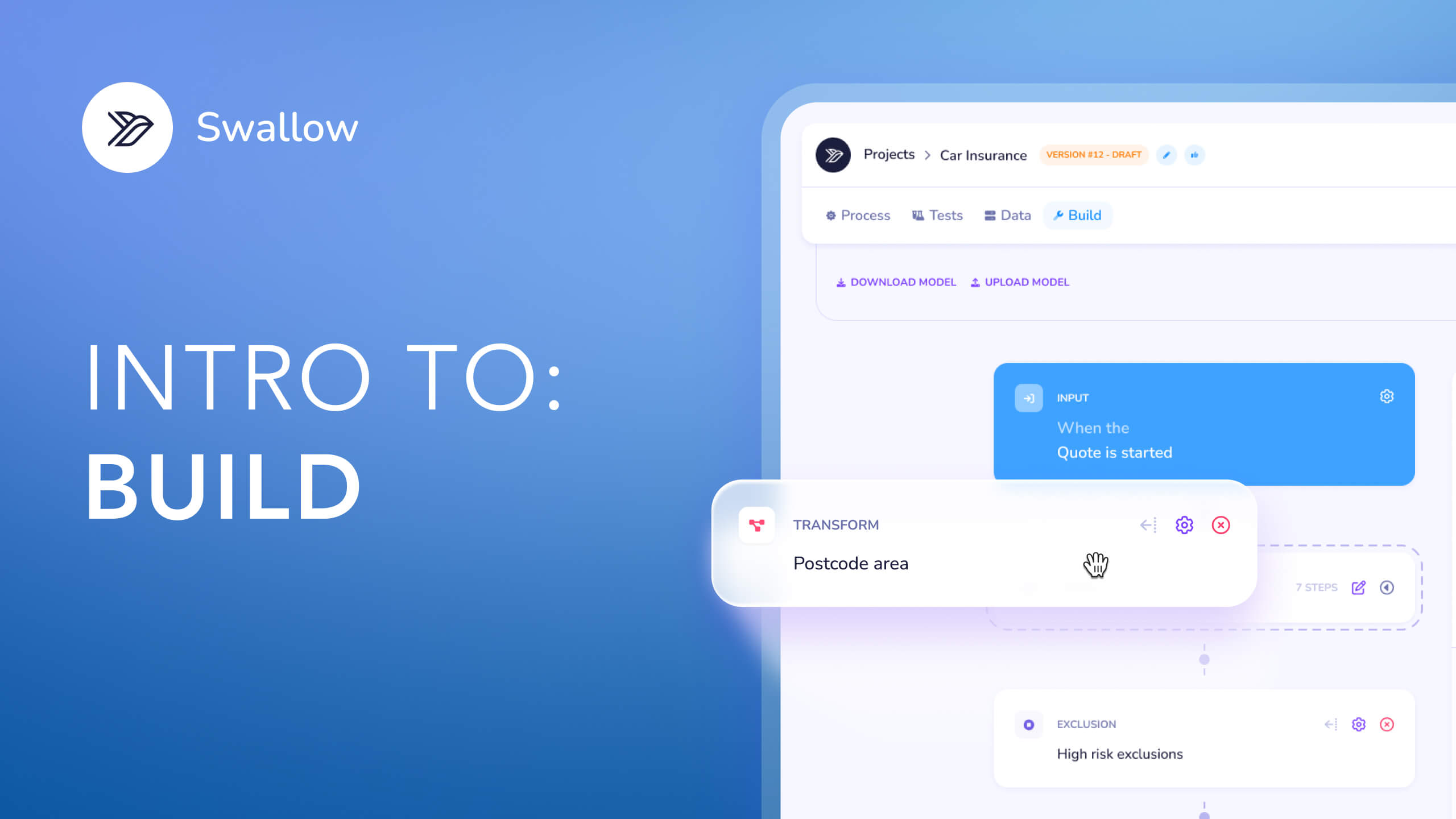

Models exist in one authoritative location and serve every distribution channel through unified APIs or forms. No fragmented spreadsheets. No duplicated logic. No channel drift.

Pricing teams define logic visually. Engineers consume high-performance APIs. Underwriters monitor decisions in real time. Everyone uses the same source of truth.

Every change, every test, every quote is logged — giving compliance teams full traceability across the pricing lifecycle.

Pricing teams deploy when ready, without being tied to slow monolithic release cycles.

Designed to handle millions of live quotes per day across multiple products and territories.

Historically, insurers wanting to replicate competitor or bureau filings needed large modelling teams and long development timelines. With a modern filings-to-model pipeline, teams can:

Instead of long build cycles, teams get a near-instant starting point that can be extended, adapted, or tested as required.

Before any rating model goes live, insurers need certainty. That’s where advanced testing capabilities come in:

This removes the risk and friction traditionally associated with pricing changes — allowing insurers to move quickly while maintaining full oversight.

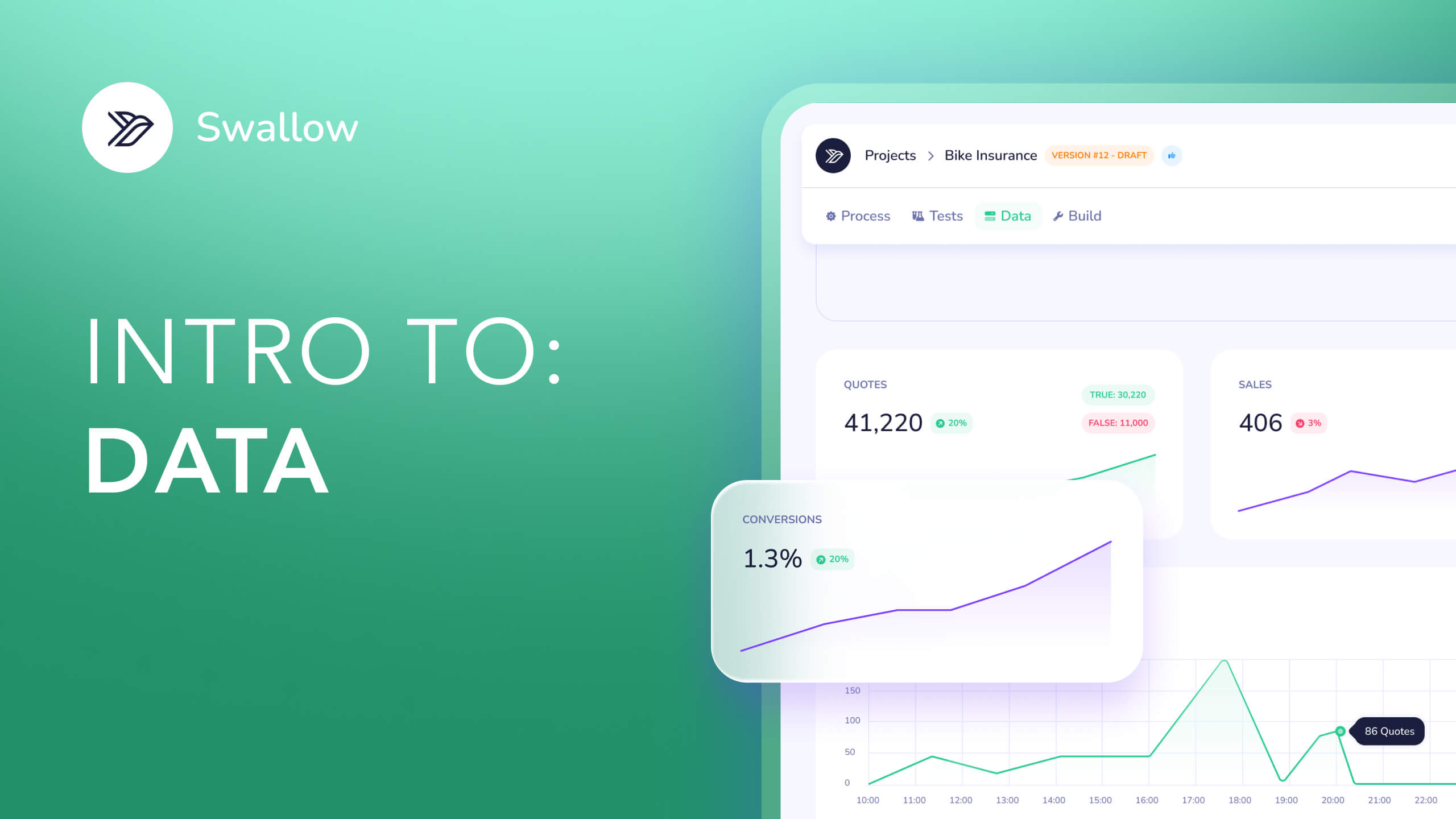

Modern pricing engines provide a live view of what is happening across the portfolio:

Insurers are no longer guessing how a model behaves in production. They can see everything, immediately.

A filings-based rating engine dramatically reduces internal effort:

Those savings compound across territories, product lines, and teams.

The market is moving faster than traditional rating systems can support. Insurers need:

Filings-based engines deliver all of this in one place — without sacrificing governance or performance.

What makes this approach powerful is not just automation. It is the combination of:

Insurers using this model aren’t just modernising their tech stack — they are transforming how pricing work gets done.

They ship faster.

They iterate with confidence.

They own their pricing future.